TL;DR

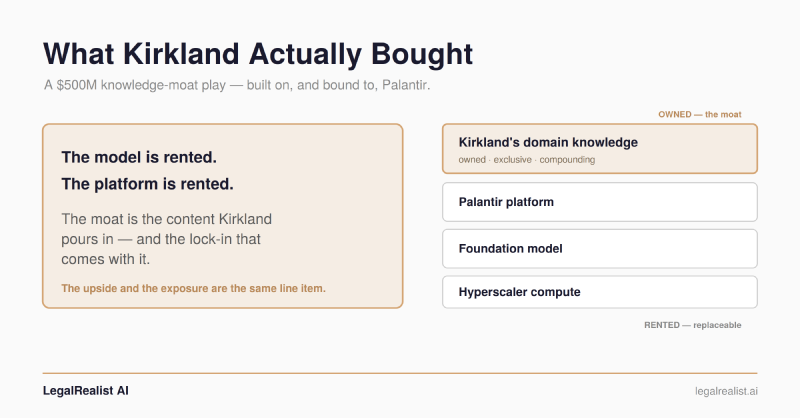

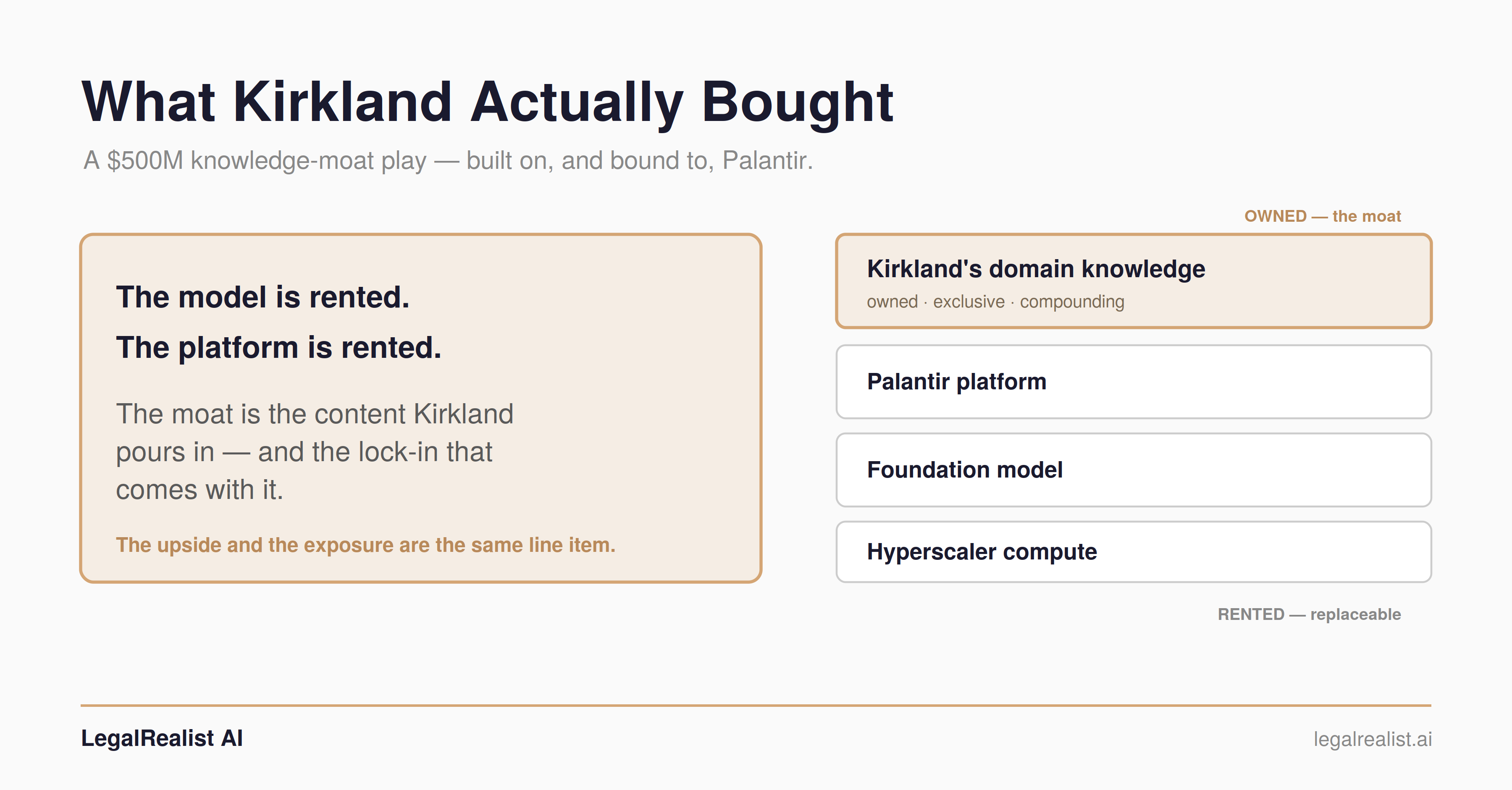

- We called the $500M an infrastructure play; it’s a knowledge-moat play built on Palantir — exclusive, model-agnostic, Kirkland-owned. A fund formation engine deep in one practice. The correction matters less than the dependency.

- Palantir’s edge isn’t the ontology — it’s integration and lock-in. Modeling data as objects is decades-old; the hard, sticky part is the plumbing. Critics call the moat “obstruction of data transfer.”

- No law-firm precedent — Kirkland is Palantir’s first. The priors are in defense, finance, and aviation, and they cut both ways: real wins and ugly exits.

- It wins if fund formation is really an integration problem. Hundreds of investors, side letters, and obligations to coordinate — at exactly the scale Palantir is built for, with depth that compounds.

- It breaks if the hard part is judgment — or if the lock-in turns the moat into a trap. The upside and the exposure are the same line item.

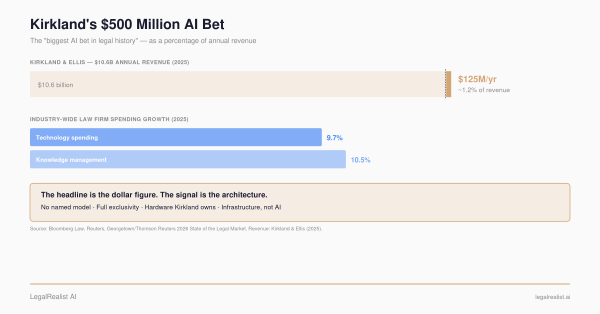

On June 4, at Palantir’s AIPCon 10 in Miami, Kirkland & Ellis put a name on its $500 million AI program: Palantir. The two unveiled a “fund formation engine” — a private-equity fundraising platform built on Palantir’s Artificial Intelligence Platform (AIP), for the 1,000-plus lawyers in Kirkland’s investment funds group.

When the $500 million was announced, we read it as an infrastructure play — owned compute, self-hosted models. The deal corrects us: it’s a knowledge-moat play, deep in one practice area, not a hardware bet. But the more useful fact is the one the headline buried — that moat is built on Palantir, and bound to it. So the way to judge Kirkland’s bet is to judge Palantir: what it actually does, what it has done before, and how those priors tend to end.

The Deal#

The fund formation engine handles the document-and-data sprawl of raising a private-equity fund: fund documentation, side-letter drafting, obligation tracking, closing commitments, compliance. It’s the first product to ship under the $500 million — not the whole program, which runs more than 180 engineers and data scientists and over 250 attorneys, including about 100 equity partners, across multiple “custom builds.” Palantir is one partnership, the flagship one.

Three terms define it. It’s exclusive — a Kirkland spokesperson confirmed Palantir can’t sell the platform to other firms. Kirkland insisted on owning the firm-specific code and data, with external partners barred from client documents. And the architecture is model-agnostic: the firm can swap the underlying foundation model without rebuilding. So this isn’t a bet on a model — the LLM is a swappable commodity underneath. The bet is on the layer above it, and on Palantir.

What Palantir Actually Brings#

Palantir owns neither the compute nor the model. Its software runs on top of the hyperscalers, and its model layer routes to the same commercial LLMs everyone rents. What it sells is a model of the domain wired to operations — the “ Ontology” — plus the governance to run it on sensitive data (granular permissions, lineage, audit logging, air-gapped deployment) and the embedded engineers who build it with you.

It’s worth being plain about the Ontology, because the word carries more brand than meaning. Stripped down, it’s object-oriented programming applied to a firm’s data. Instead of leaving the facts as rows in a database — one table of funds, one of investors, one of side letters, joined by ID — the Ontology defines the real things and how they behave: a fund and a side letter become types (like classes in code), each with properties (a side letter has an investor, a fund, an MFN tier, a date), links to one another, and actions you can run on them (mark an obligation satisfied, assemble a closing checklist), each action limited to the right roles. A read-only “semantic layer” lets you query data in plainer terms; an Ontology lets applications and an LLM act on it, against defined objects instead of a pile of raw files.

But is that Palantir’s edge? Not really — and the skepticism is healthy. Modeling data as objects is decades-old computer science, and the “semantic layer” category is now crowded with Snowflake, Databricks, Microsoft, and Salesforce. What Palantir really sells is the integration to build the model — and the switching costs once you have. Michael Burry has argued the moat is mostly “obstruction of data transfer” — lock-in dressed up as IP. The rebuttal is that once a firm’s workflows, permissions, and decisions live inside the model, leaving means rebuilding years of work. Both can be true: what looks like a deep moat from one side looks like a trap from the other.1 Either way, the framework is rented; what isn’t rentable is what Kirkland pours in — its own fund-formation work — and the advantage that creates is inseparable from the lock-in that comes with it.

Palantir’s Track Record#

Palantir has never done this for a law firm. Kirkland is its marquee entry into legal — the company built its business on government and defense work and has no law-firm precedent to point to. So the only way to handicap the bet is by analogy, and the analogies cut both ways.

On the win side, Palantir’s commercial track record is in regulated, entity-heavy data: anti-money-laundering for banks like Société Générale, a 2026 trial across the UK financial regulator’s data lake covering 42,000 firms, and operational platforms at scale like Airbus’s Skywise, used by 25,000-plus people across airlines. These show Palantir can integrate sprawling, sensitive data and make it operational — and, with Skywise, that the result can stick and scale for years.

On the loss side, the failures rhyme. The NYPD used Palantir for five years, couldn’t easily extract its own analytical work when it wanted out, built a replacement, and left. Former Treasury officials warned that the IRS’s reliance on Palantir risks “capture” and technical lock-in. The UK NHS deployment drew lawsuits and patient opt-outs over data governance. None of these is the technology failing to work. They’re the relationship souring, the bottleneck turning out to be something other than integration, or the lock-in becoming the story.

How Kirkland’s Bet Wins#

Palantir’s wins share a shape: a high-stakes, coordination-heavy problem where bad coordination is catastrophic, and an organization with the budget, will, and stability to embed the platform and rebuild its workflows around it. When those align, the integration value dwarfs the price and the system becomes the organization’s operating memory.

Fund formation can fit that shape. A single fund involves hundreds of investors, each with a side letter of bespoke terms, and obligations that must be tracked for the life of the fund and cross-referenced against one another — a most-favored-nation term granted to one investor may have to be offered to others. That is a coordination-and-integration problem at the scale Palantir is built for. Kirkland has the budget, the will — about 100 equity partners helped shape the platform — and a franchise lucrative enough to justify the embed. If the binding constraint really is structuring and tracking that web, and if the firm’s accumulated fund-formation knowledge compounds inside the model the way its CTRAN deal database has for years, Kirkland gets a moat no competitor can replicate by licensing the same software. That is the knowledge-moat thesis, realized — and it is genuinely Kirkland’s, because the content is Kirkland’s.

How It Breaks#

Palantir’s failures come in three shapes, and each maps onto a Kirkland risk.

The bottleneck might be the wrong one. Palantir wins when the hard part is integration; it disappoints when the hard part is judgment, or when cheaper software would have done. Fund formation is half integration (obligations and data — a fit) and half bespoke legal judgment (drafting and negotiating terms — not a fit, and the part the swappable model handles, where Hallucination risk lives). If most of the value is in the judgment, Kirkland has bought expensive plumbing for a problem that wasn’t plumbing.

The firm might not sustain it. Palantir’s model demands continuous engineering and real workflow change; deployments wither when budgets tighten, leadership turns over, or the organization won’t restructure around the tool. Partnerships are notoriously hard to march in lockstep, and law-firm knowledge management has failed for years for a simple reason — the benefit is collective, the cost individual. If partners don’t adopt it, the platform decays into shelfware.

The lock-in might turn toxic — but this is the pitfall Kirkland is best-equipped to dodge. The moat is tied to Palantir, and if the firm can’t lift its Ontology and content off the platform, the moat belongs to the vendor, not the firm. Yet Kirkland is a firm of elite dealmakers, and Palantir’s record of stranding partners — the NYPD most of all — is exactly the precedent it would have studied before signing. The smart structure writes in optionality: rights to cancel and to scale up or down, and contractual portability of the firm’s data and Ontology, not just its code. The reporting confirms Kirkland owns its code and data but says nothing about exit or portability terms; which of those Kirkland secured is the difference between a hedged bet and a trap. Separately, Palantir carries reputational freight — its tools’ use in government surveillance and immigration enforcement — that some clients and laterals will weigh regardless of the technology.

What We’re Watching#

Three variables decide which Palantir story Kirkland becomes. Whether fund formation is really an integration problem (it wins) or a judgment problem (it doesn’t). Whether the firm sustains adoption across a partnership. And whether Kirkland’s ownership of its code and data is portable enough to make the moat its own rather than Palantir’s.

It is still a knowledge-moat play — deep, domain-specific, the kind of advantage that compounds. But it is a knowledge moat built inside someone else’s platform, which means Kirkland’s upside and its exposure are the same line item. The firm seems to understand that: the exclusivity, the owned code and data, the hundred partners in the room read like a firm negotiating the terms of a marriage it knows it is entering. Whether those terms hold is the thing to watch.

Further Reading#

- Palantir and Kirkland & Ellis Partner to Transform Private Equity Fundraising. The joint announcement.

- Kirkland’s $500 Million AI Gambit Requires a Cast of Hundreds. Bloomberg Law on the team behind the program and the model-agnostic architecture.

- Kirkland, Palantir Launch AI Tool Targeting Fund Formation. Bloomberg Law on exclusivity and the inflection-point framing.

- Palantir’s Moat Is Just “Obstruction of Data Transfer,” Michael Burry Says. The lock-in critique, with the NYPD example.

- AIP Architecture Overview. Palantir’s documentation on supported models and managed infrastructure.

- Palantir Contracts Under Scrutiny Amid IRS Tax Data Controversy. Tax Notes on capture and lock-in risk.

- Kirkland’s $500 Million AI Bet. The earlier analysis this post corrects.

- Buy, Build, or Partner: Three BigLaw Bets on AI. Part 1: the strategy framework.

This post is part of the Law Firm AI Positioning series on LegalRealist AI. It extends and corrects an earlier analysis in light of the June 4, 2026 Kirkland–Palantir announcement. It is intended for informational and educational purposes only and does not constitute legal advice. AI capabilities, pricing, and market conditions described here reflect publicly available information as of the publication date and are subject to rapid change. Kirkland & Ellis has not disclosed the full technical architecture of its platform; the analysis here is based on publicly reported details and industry context.

The lock-in is structural, not incidental. Because each deployment carries the fixed cost of embedded engineers, the model only pays off on large, long-retention contracts — so it depends on high switching costs to defend its own economics. That makes Palantir a high-variance choice: transformative when the problem really is integration and coordination in a high-stakes, stable, well-funded setting, and an expensive, sticky mistake when it isn’t. It’s a marriage, not a purchase, and the clients who fare worst are the ones who didn’t treat it as one. Read that way, Kirkland’s exclusivity terms and its insistence on owning its own code and data look like negotiating the divorce up front. The NYPD didn’t. ↩︎

{kind=link}

{kind=link}

{kind=link}