Editor’s note (June 2026): This post read Kirkland’s $500 million commitment as an infrastructure play — owned compute, self-hosted open-weight models. The June 4, 2026 Kirkland–Palantir announcement showed that read was wrong: the program is a knowledge-moat play built on Palantir’s platform, not a hardware bet. The corrected analysis is in What Kirkland Actually Bought. The original text is preserved below.

TL;DR

- This is an infrastructure play that enables two things no rented stack can: a compounding knowledge moat and a fixed-fee billing model. Kirkland declined to name a foundation model provider and barred outside builders from reselling. Those aren’t AI decisions — they’re infrastructure decisions.

- It’s also the lowest-risk option on the board. The hardware is a depreciable capital asset with resale value. The software is wrappers — prompt libraries, retrieval pipelines, UI — not novel R&D. DeepSeek, Meta, and Moonshot already did the hard part and released it under MIT licenses.

- The full stack is now possible. DeepSeek V4 Pro and Kimi K2.6 — both open-weight and frontier-competitive — shipped weeks before the announcement. Self-hosted inference at Kirkland’s volume is cheaper, private, and no longer a performance compromise.

- This is a subsidy cliff hedge. Owning inference converts variable token cost — set by providers who call their own pricing “accidental” — into fixed infrastructure Kirkland controls.

- CTRAN is the precedent — and the moat is the point. Kirkland builds proprietary infrastructure when the data compounds into competitive advantage. The AI platform follows the same logic: every matter processed on owned hardware trains a system competitors can’t replicate by buying the same vendor license.

- The infrastructure enables a billing model no rented stack can support. A firm that owns its inference knows its cost per document to the penny — the prerequisite for fixed-fee pricing PE clients have demanded for a decade. No firm whose largest variable cost is set by someone else’s pricing decisions can make the same guarantee.

Corrections & Updates

- June 7, 2026 (model update): Then-current comparison points were Claude Opus 4.8 ($5/$25 per million tokens) and GPT-5.5 ($5/$30); the forward-looking “subscribe to Claude Opus or GPT-5” reference was updated accordingly. The benchmark comparisons to Opus 4.6/4.7 and GPT-5.4 are left as accurate point-in-time results from each model’s spring-2026 release.

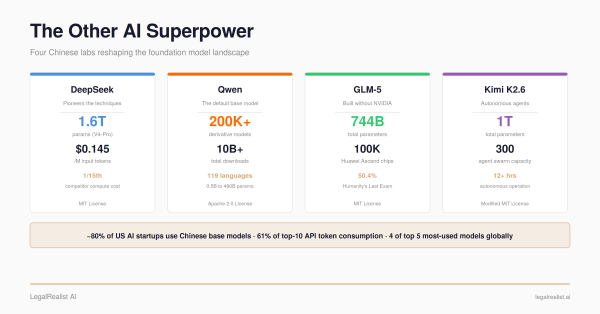

On April 20, 2026, Moonshot AI released Kimi K2.6 — a one-trillion-parameter

open-weight model that beat Claude Opus 4.6 on SWE-Bench Pro by 5.2 points. Four days later, DeepSeek shipped V4 Pro — 1.6 trillion parameters, MIT license, within 0.2 points of Claude Opus on SWE-bench Verified, at a tenth to a thirtieth of the per-

Token cost. Both self-hostable on enterprise hardware.

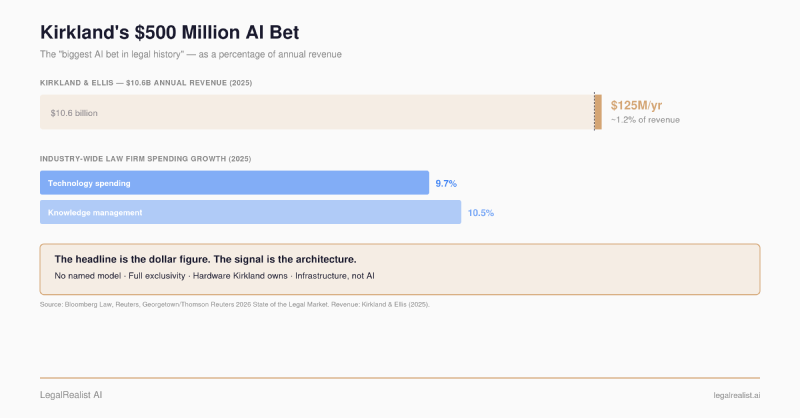

Five weeks after that, Kirkland & Ellis committed $500 million to build a proprietary AI platform — and declined to name which Foundation Model it would run on.

Every headline called it an AI bet. The signals in the announcement point to something else.

What Kirkland Announced#

On May 28, 2026, Kirkland & Ellis committed $500 million over three to four years to develop what it describes as a proprietary AI platform. The firm will spend over $100 million in 2026 alone, funded entirely from revenue. 250 of the firm’s lawyers — including 100 partners — shaped the platform’s design. More than 180 technology professionals, inside and outside the firm, are building it. Outside technology firms involved in construction will not be permitted to resell the resulting technology. Kirkland will continue licensing some third-party AI programs. Chair Jon Ballis hinted that AI would accelerate a shift toward value-based pricing, saying the firm was “looking forward to leaning into it.”

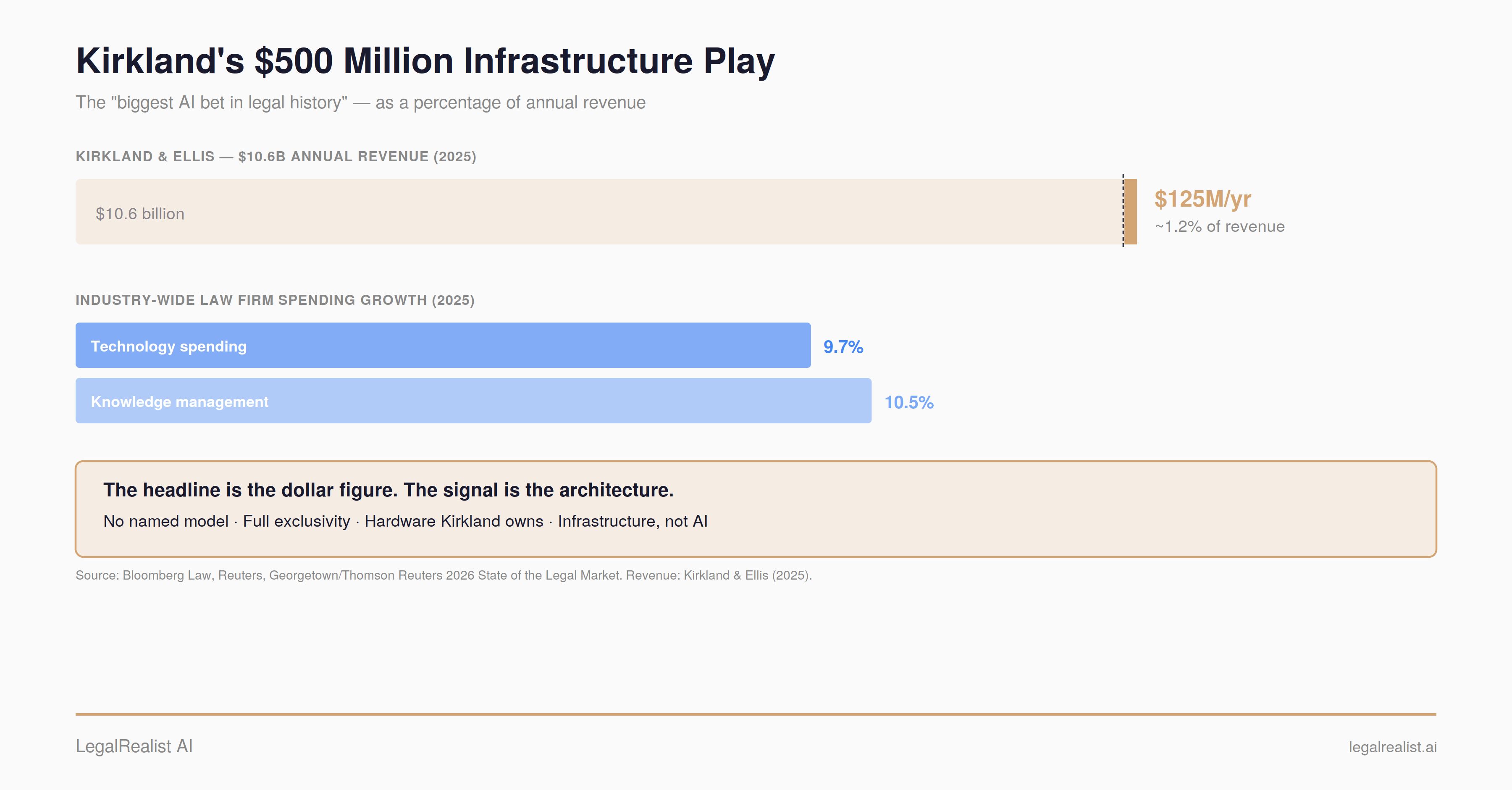

The revenue context matters. Kirkland generated $10.6 billion in 2025 — the first law firm to break the $10 billion barrier — with profit per equity partner at a record $11.1 million. $500 million over four years is roughly $125 million per year, or about 1.2% of annual revenue. Industry-wide law firm technology spending grew 9.7% in 2025, the fastest rate ever recorded, with knowledge management costs up 10.5%. At Kirkland’s scale, 1.2% barely outpaces the industry average.

What Everyone Else Said#

The Financial Times broke the story. Reuters, Bloomberg Law, and Law360 followed within hours. The coverage converged on a single frame: “AI bet.” The largest AI investment in legal history. An “AI arms race.” A “$500 million AI platform to leverage the firm’s collective intelligence.”

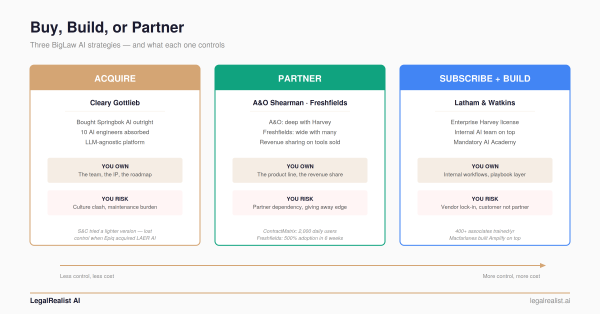

The comparisons drawn were to other AI strategies: Freshfields’ multi-year collaboration with Anthropic, A&O Shearman’s co-development deal with Harvey, Latham’s enterprise Harvey license. All fair comparisons — we profiled all three in an earlier post. But every one of those strategies names a Foundation Model partner. Kirkland didn’t.

That absence is the signal the AI framing missed.

The Infrastructure Read#

Two details in Kirkland’s announcement point away from “AI strategy” and toward infrastructure play.

No named model. Every BigLaw AI strategy in our earlier survey of the field named its Foundation Model partner. A&O Shearman built with Harvey. Freshfields partnered with Anthropic and Google. Latham licensed Harvey firmwide. Kirkland declined to say whether its platform would rely on a specific generative AI model. If the platform is built to run open-weight models on Kirkland’s own hardware, there is no Foundation Model partner to name — just infrastructure the firm owns.

Full exclusivity. Outside technology firms building the platform cannot resell it. Compare to Freshfields, whose Anthropic deal explicitly allows Anthropic to sell co-developed products to rival firms. Kirkland’s exclusivity clause means whatever gets built produces advantages that stay internal.

Read together: Kirkland is building compute infrastructure, data pipelines, retrieval systems, and Application Layer workflows — infrastructure that runs on models it can swap without renegotiating a vendor contract. The AI is the software that runs on the infrastructure. The infrastructure is the investment.

That distinction matters twice. First, infrastructure is a fixed cost Kirkland controls — the prerequisite for fixed-fee pricing that no firm renting tokens can offer. Second, infrastructure that processes client data internally means the institutional knowledge built on that data — prompt libraries, retrieval indices, Fine-Tuning — stays inside the firm and compounds with every matter. A competitor licensing Harvey gets Harvey’s generic capabilities. Kirkland gets a system trained on Kirkland’s work.

The Risk Profile Nobody Mentioned#

The coverage treated $500 million as a high-stakes gamble. Measured against the other BigLaw AI strategies, it’s the lowest-risk option on the board.

The hardware is a capital asset — though one that depreciates faster than most. GPU generations turn over every 12–18 months, and resale values drop accordingly. That’s a real cost, and Kirkland should expect to refresh hardware on a cycle closer to laptops than to office buildings. But the current seller’s market for Inference compute keeps floor values higher than historical norms, and the hardware can be leased to third parties if Kirkland’s internal demand changes. If the AI thesis collapses entirely — an unlikely but useful stress test — Kirkland owns servers it can sell at depreciated value. Cleary owns a team it has to retain. A&O Shearman owns a revenue-share agreement with a startup whose roadmap it doesn’t control.

The software layer is similarly bounded. Kirkland isn’t training a Foundation Model — that’s billions of dollars of R&D that DeepSeek, Meta, and Moonshot have already done and released under MIT licenses. What Kirkland is building is the Application Layer: prompt libraries, retrieval pipelines, workflow orchestration, user interfaces — wrappers that connect existing models to the firm’s documents and lawyers. This is the same category of work that a five-person engineering team at a midsize firm does on a Harvey subscription. Kirkland is doing it at larger scale with more resources, not doing something categorically different.

The $500 million buys infrastructure with residual value and software with bounded complexity. That’s a less risky profile than acquiring a company, co-developing with a startup, or — for that matter — committing to a multi-year enterprise license with a vendor that might get acquired, reprice, or pivot before the contract expires.

The Full Stack Is Now Possible#

This announcement couldn’t have happened eighteen months ago. The open-weight models available in late 2024 trailed closed-source frontier models by margins that mattered on complex legal work. That gap has closed.

DeepSeek V4 Pro, released April 24, 2026: 1.6 trillion total parameters, 49 billion active per forward pass, MIT license, self-hostable. It scores within 0.2 points of Claude Opus on SWE-bench Verified and matches GPT-5.5 and Claude Opus 4.7 on most

agentic

benchmarks at roughly a tenth to a thirtieth of the per-

Token cost. One million

input tokens costs $0.14 on V4-Flash.

Kimi K2.6, released April 20, 2026: one trillion parameters, open-weight, beating Opus 4.6 on SWE-Bench Pro by 5.2 points and GPT-5.4 on Humanity’s Last Exam with tools. It scales to 300 sub-agents executing 4,000 coordinated steps — the kind of multi-step orchestration that

agentic legal workflows demand.

The Foundation post in our Legal AI Landscape series tracked the open-weight/closed-source performance gap narrowing from roughly 18 percentage points in late 2023 to essentially zero on knowledge and reasoning benchmarks by early 2026. For the high-volume transactional work that defines Kirkland’s practice — contract extraction, due diligence triage, document classification, summarization — the open-weight frontier isn’t approaching sufficiency. It has arrived.

Kirkland can still subscribe to Claude Opus 4.8 or GPT-5.5 for the hardest tasks — novel legal reasoning at the boundary of model capability, complex multi-step

agentic workflows,

Multimodal analysis. But those are optional subscriptions layered on top of infrastructure Kirkland owns. Every time the next

open-weight release closes another gap, Kirkland pulls more volume off rented APIs and onto its own hardware — without changing a workflow, without renegotiating a contract. The dial only turns one direction.

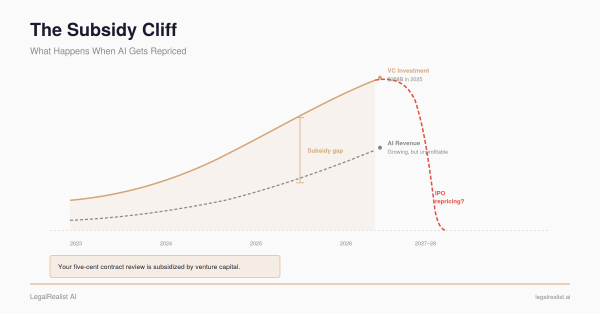

Pricing In the Subsidy Cliff#

In March 2026, The Subsidy Cliff made the case that every major AI lab prices Inference below cost, and that firms building workflows around today’s API prices are building on someone else’s venture capital. OpenAI projects $14 billion in losses for 2026. OpenAI’s head of ChatGPT called the company’s pricing model “accidental” and said there’s “no world in which pricing doesn’t significantly evolve.” Both OpenAI and Anthropic are expected to IPO by late 2026 or 2027 — and public markets don’t reward market share at any cost.

The Subsidy Cliff post identified the self-hosted Inference break-even at roughly 50 million tokens per day. Above that threshold, firms save 50–70% versus API pricing. Below it, the fixed costs of self-hosting exceed what you’d pay through an API.

Kirkland’s daily Token consumption — thousands of lawyers, PE deals involving thousands of documents per transaction, due diligence pipelines that process entire data rooms — almost certainly exceeds that threshold by a wide margin. At Kirkland’s volume, self-hosted Inference on open-weight models isn’t a compromise. It’s cheaper, it’s private, and the cost doesn’t change when a provider decides its pricing was accidental.

The $500 million converts Kirkland’s largest variable AI cost into fixed infrastructure. No API repricing risk. No 90-day rate change notices. No dependency on a provider’s venture capital runway. Kirkland knows what Inference costs per document, per matter, per year — and that number doesn’t change with someone else’s pricing decisions. That cost certainty is one half of the endgame. The other half is what happens to the data flowing through that infrastructure: it stays inside the firm, compounds into institutional knowledge, and builds the moat the next section describes.

The Knowledge Moat#

CTRAN isn’t evidence that Kirkland can build AI. It’s evidence that Kirkland builds proprietary infrastructure when the data compounds into competitive advantage — and that the moat is the point.

CTRAN is Kirkland’s proprietary M&A transaction database, recognized by the Financial Times as a “standout” in its 2017 Innovative Lawyers report. It collects data on past deals — terms, structures, negotiation outcomes — and gives Kirkland’s corporate lawyers real-time trend intelligence no competitor can replicate. The value isn’t the software. It’s the data accumulated over thousands of transactions. SideTrack applies the same logic to investment fund formation. Both were built internally because sending that data to a third-party platform would mean sharing the competitive advantage with anyone else who licenses the same vendor.

The AI platform follows the same pattern at a different layer. Client documents processed on Kirkland’s own hardware never leave the firm’s perimeter. No third-party API terms to negotiate, no data processing agreements to audit, no provider terms-of-service change to monitor. For PE clients who care intensely about where their deal documents go — and who represent the core of Kirkland’s revenue base — this eliminates the conversation entirely. (For the privilege and data retention analysis, see The Foundation’s coverage of ABA Opinion 512 and API data policies.)

The compounding question is whether the institutional knowledge built on top of the models — prompt libraries, Fine-Tuning on Kirkland’s work product, retrieval indices tuned to its document types — accumulates the way CTRAN’s deal-term data does. If prompt libraries and RAG configurations get more valuable with every matter processed, the infrastructure investment self-reinforces. If each Foundation Model generation resets the Application Layer, the infrastructure needs continuous rebuilding. CTRAN’s track record suggests Kirkland knows how to make proprietary data compound. Whether that transfers to the AI layer is the open question — but if it does, the combination is potent. A firm that owns its Inference (predictable cost) and has a self-reinforcing knowledge layer (better output than competitors on the same document types) can offer fixed-fee pricing at margins that improve over time. That’s the endgame the next section describes.

From Infrastructure to Fixed Fees#

The infrastructure play produces two advantages that reinforce each other. Owned Inference gives Kirkland predictable cost per document. The knowledge moat — prompt libraries, Fine-Tuning, retrieval indices trained on thousands of matters — gives Kirkland better output on the document types its clients bring. Predictable cost plus superior output equals fixed-fee pricing at controlled margins that improve with every deal.

Ballis said Kirkland is “looking forward to leaning into” value-based pricing. The infrastructure is what makes that transition mechanically possible — and without it, the pricing shift can’t happen. A firm that knows its cost per document — a fixed number based on hardware it owns — can price a due diligence review, a contract analysis, or a fund formation at a fixed fee with controlled margins. No firm renting tokens at rates set by a provider whose head of product called its own pricing “accidental” can offer the same guarantee.

PE clients have pushed for fee predictability for a decade. A firm that can quote a fixed price for due diligence — because it controls every variable in the cost stack — has a structural advantage over firms still guessing at their per- Token costs. This isn’t “AI makes lawyers faster.” Every firm gets that. It’s “AI on infrastructure we own makes our cost structure legible enough to price work the way clients have been asking us to.”

Kirkland has disrupted legal market structure before. It built the modern PE law practice by reorganizing around deal volume and speed when competitors were still structured around practice-area silos. Fixed-fee delivery on a self-hosted AI stack is the same instinct applied to the next structural shift: the firm that can price legal work with the precision of a fixed-cost operation gains a structural advantage in every pitch, every panel review, every beauty contest.

The counterweight is real. $11.1 million PPP is built on hourly rates and leverage — large associate teams billing premium rates on high-stakes transactions. A billing model transition requires partners to accept lower per-unit revenue in exchange for higher volume and predictability. The Georgetown/Thomson Reuters 2026 State of the Legal Market report warned that firms are “spending like current conditions represent permanence rather than a temporary spike.” Kirkland’s bet is that it can build the new model before the old one stops working — and that the infrastructure to do so costs $500 million.

What This Means for Everyone Else#

Most firms won’t replicate the full play. They don’t need to. But any firm that’s bullish on AI — that plans to run more of its practice through LLM-powered workflows next year than this year — should own some of the stack before subsidy pricing ends. The tightening has already started. Google has imposed usage caps on Gemini that didn’t exist six months ago. OpenAI called its own pricing “accidental.” Anthropic has signaled rate adjustments. The question isn’t whether repricing happens — it’s whether you have alternatives when it does.

A 25-lawyer litigation firm doesn’t need $500 million in GPU clusters. Kirkland is spending 1.2% of revenue. A firm doing $10 million a year could spend $50,000–$100,000 on a single server running a smaller open-weight model and handle high-volume routine work — contract classification, document summarization, email triage — without an API meter running. The subscribe-and-build model from Part 1 remains the right starting point. The hedge is adding a self-hosted layer underneath it, so that when a provider reprices or caps usage, the firm’s core workflows don’t stop.

If Kirkland is right that owning Inference is the endgame, every legal AI vendor built on third-party APIs faces the same repricing exposure it sells clients insurance against. The vendors with durable value are the ones selling Application Layer work that’s hard to replicate — domain-specific workflows, retrieval pipelines tuned to specific document types, evaluation frameworks — not reselling someone else’s tokens at a markup. Harvey, Legora, and the rest of the legal AI market should be reading Kirkland’s announcement less as a lost customer and more as a signal about where margins will compress.

What to Watch#

Model disclosure. If Kirkland confirms self-hosted open-weight models as the platform’s base, this is an infrastructure story and the economics are replicable at sufficient scale. If it’s primarily closed-source APIs behind a proprietary Application Layer, the $500 million bought a very expensive version of what Latham built for a fraction of the price.

The ratio. What share of Kirkland’s Inference runs on local hardware versus through frontier API subscriptions — and which direction that split moves. Every open-weight release that closes another capability gap makes Kirkland’s owned infrastructure more valuable and its rented subscriptions more optional.

Knowledge compounding. If Kirkland reports that its AI system’s accuracy or speed improves measurably with each quarter of accumulated matter data — the way CTRAN’s deal-term intelligence improved with each transaction — the moat thesis is validated. If each Foundation Model update resets the Application Layer and requires rebuilding from scratch, the compounding advantage is weaker than the CTRAN analogy suggests.

Pricing model. Fixed-fee or value-based arrangements growing as a share of Kirkland’s revenue would confirm the infrastructure-to-billing thesis. If hourly billing stays dominant, the platform supplements the existing model rather than enabling a new one.

Subsidy cliff timing. The Subsidy Cliff post projected 30–50% API price increases within 18 months. If that materializes while open-weight performance keeps improving, Kirkland’s timing looks prescient. If efficiency gains and competition hold API prices flat, the urgency of self-hosting diminishes — but Kirkland still owns depreciable hardware with resale value, not a sunk software investment.

Peer response. Similar infrastructure commitments from other top-10 firms would validate the thesis. Doubling down on vendor partnerships would mean the market has decided that the infrastructure play only works at $10.6 billion in revenue — and that Kirkland is an outlier, not a leading indicator.

Further Reading#

- Kirkland & Ellis Investing $500 Million to Build AI Platform. Bloomberg Law’s coverage of the announcement.

- Law Firm Kirkland to Spend $500 Million Developing Its Own AI Platform. Reuters’ reporting on the investment and industry context.

- Kirkland & Ellis Has Form for Building Its Own Technology. Legal IT Insider’s analysis, including the CTRAN precedent and Freshfields comparison.

- DeepSeek V4: Features, Benchmarks, and Comparisons. DataCamp’s technical overview of V4 Pro and Flash.

- Kimi K2.6 Complete Guide. Walkthrough of Moonshot AI’s open-weight agentic model.

- Buy, Build, or Partner: Three BigLaw Bets on AI. Our earlier piece: the three-strategy framework for BigLaw AI positioning.

- The Subsidy Cliff: What Happens When AI Gets Repriced. The token pricing thesis Kirkland appears to be acting on.

- Self-Hosted LLMs vs. API-Based LLMs: Cost Performance Analysis. Break-even analysis for self-hosted versus API inference.

- Legal Tech Spending Surges 9.7%. The 2026 Georgetown/Thomson Reuters State of the US Legal Market report.

- The Legal Market at a Crossroads. Thomson Reuters on the five forces reshaping law firm economics.

This is a standalone post on LegalRealist AI. It is intended for informational and educational purposes only and does not constitute legal advice. AI capabilities, pricing, and market conditions described here reflect publicly available information as of the publication date and are subject to rapid change. Kirkland & Ellis has not disclosed the technical architecture of its platform; the analysis in this post is based on publicly reported details and industry context.

{kind=link}

{kind=link}

{kind=link}